Fill Your Cg 20 10 07 04 Liability Endorsement Form

Fill Your Cg 20 10 07 04 Liability Endorsement Form

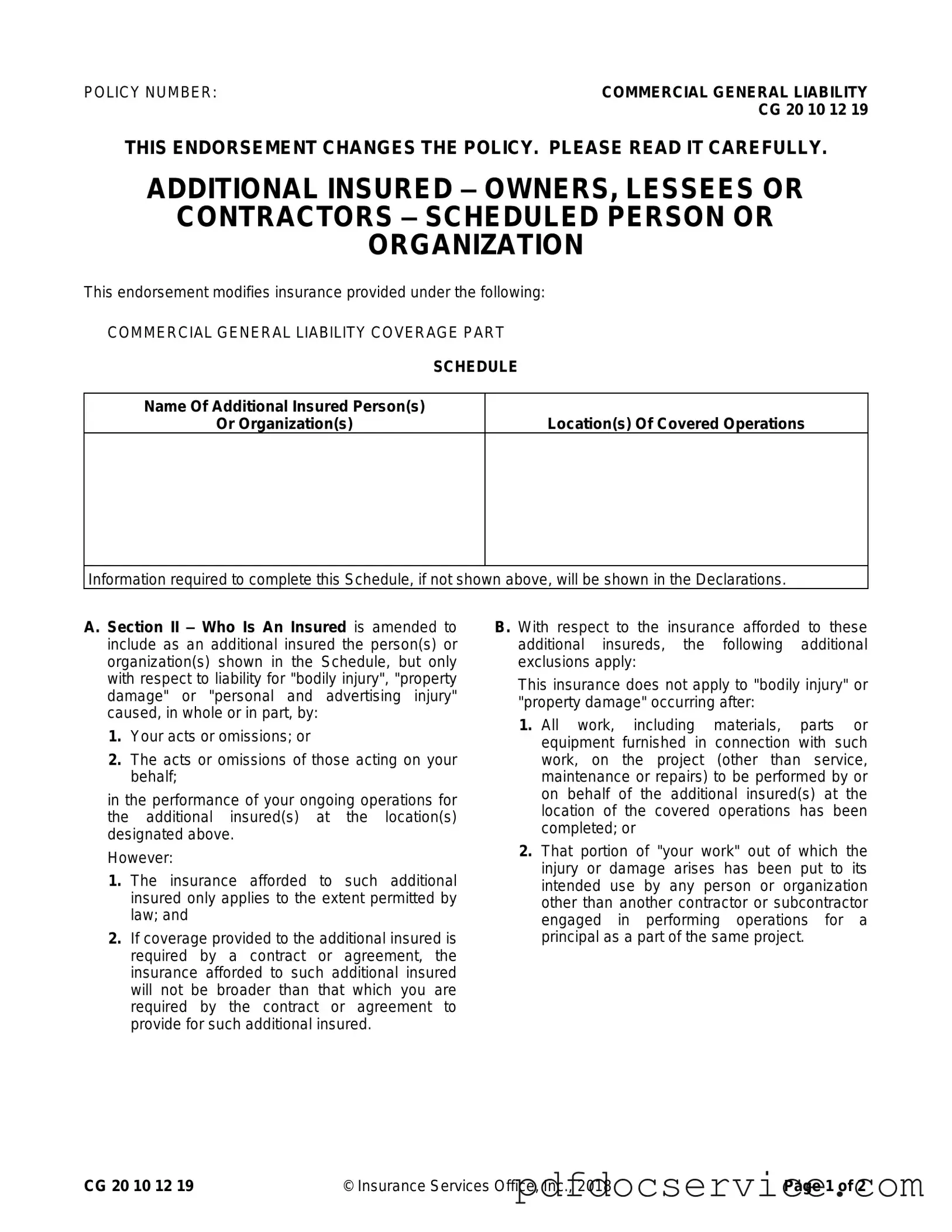

The CG 20 10 07 04 Liability Endorsement form plays a crucial role in the realm of commercial general liability insurance, particularly when it comes to defining the responsibilities and protections afforded to various parties involved in a project. This endorsement specifically adds additional insured status for owners, lessees, or contractors named in a scheduled list, ensuring they are covered for certain liabilities that may arise during ongoing operations. It is essential for businesses to understand that this coverage is contingent upon the actions of the insured party or those acting on their behalf, and it only applies to specific types of injuries or damages. Moreover, the endorsement outlines important limitations, such as the exclusion of coverage for injuries or damages occurring after the completion of work, which underscores the importance of timing in liability claims. Additionally, if a contract stipulates a certain level of coverage for the additional insured, the endorsement will not extend beyond those requirements, thereby maintaining a clear boundary on the extent of liability. By grasping these key aspects, businesses can better navigate their insurance needs and ensure they are adequately protected against potential risks associated with their operations.

Operating Agreement: This document is essential for LLCs, as it outlines management structures and procedures. For more details on creating an Operating Agreement, visit https://mypdfform.com/blank-operating-agreement.

| Fact Name | Description |

|---|---|

| Policy Number | This endorsement is identified by the policy number CG 20 10 12 19, indicating its specific coverage provisions. |

| Additional Insured Coverage | The endorsement allows for additional insureds, such as owners, lessees, or contractors, to be included in the policy under specific conditions. |

| Coverage Limitations | Insurance coverage for additional insureds is limited to the extent required by law or by contractual agreements. |

| Exclusions | Bodily injury or property damage claims are excluded if they occur after the completion of work or when the work has been put to its intended use. |

| Governing Law | This endorsement is subject to state-specific laws, which may vary by jurisdiction. Always consult local regulations for applicability. |

Completing the CG 20 10 07 04 Liability Endorsement form is essential for ensuring that the necessary parties are covered under your commercial general liability policy. Accurate and timely submission of this form is crucial to maintain compliance and protect your interests. Follow the steps below to fill out the form correctly.

When filling out and using the CG 20 10 07 04 Liability Endorsement form, consider the following key takeaways:

Car Repair Estimate Template - List any safety features or systems that need checking.

To manage your vehicle matters effectively, consider utilizing the Motor Vehicle Power of Attorney form, which provides you the ability to delegate authority for registration and title transfer tasks, making it easier for you to handle these responsibilities. For more information, check out this link: important motor vehicle power of attorney resources.

Chick Fil a - Eager to represent a respected and beloved brand.

The CG 20 10 07 04 Liability Endorsement form is an important document in the realm of commercial general liability insurance. It adds additional insured parties to the policy, which can help protect them from certain liabilities. Along with this endorsement, several other forms and documents are often used to ensure comprehensive coverage and clarity in contractual agreements. Here is a list of commonly associated documents.

These documents work together to provide a clear framework for insurance coverage and liability management. Understanding each document's role can help ensure that all parties are adequately protected and informed throughout the contractual relationship.

The CG 20 10 07 04 Liability Endorsement form is an addition to a Commercial General Liability policy. It allows certain individuals or organizations to be named as additional insureds. This means they receive some level of coverage under your liability insurance for specific incidents related to your work.

You can add owners, lessees, or contractors as additional insureds. The specific names and organizations must be listed in the endorsement. This helps ensure they are covered for liabilities that may arise from your operations.

This endorsement covers liabilities related to "bodily injury," "property damage," or "personal and advertising injury." However, the coverage applies only if these incidents are caused by your actions or those acting on your behalf during ongoing operations.

Yes, there are limitations. The coverage only applies to the extent allowed by law. Additionally, if a contract specifies the coverage, it cannot exceed what the contract requires. This ensures that the coverage aligns with any agreements you have made.

There are specific exclusions to note:

The limit of insurance for additional insureds is determined by the lesser of two amounts: the amount required by your contract or the available limits of your insurance. This means that the coverage does not increase the overall limits of your policy.

Yes, you typically need to notify your insurance company to add someone as an additional insured. They will need the necessary details to update your policy and issue the endorsement.

Yes, you can add multiple additional insureds. Each one must be listed in the endorsement. Make sure to provide the correct names and any specific locations related to their coverage.

If the additional insured has their own insurance, your policy may still provide coverage for them. However, the endorsement does not change their own insurance obligations. They should still rely on their policy for coverage when applicable.

There may be an additional cost to add an additional insured to your policy. It depends on your insurance provider and the specifics of your policy. Always check with your insurer for details on any potential fees.