Blank Deed in Lieu of Foreclosure Form

Blank Deed in Lieu of Foreclosure Form

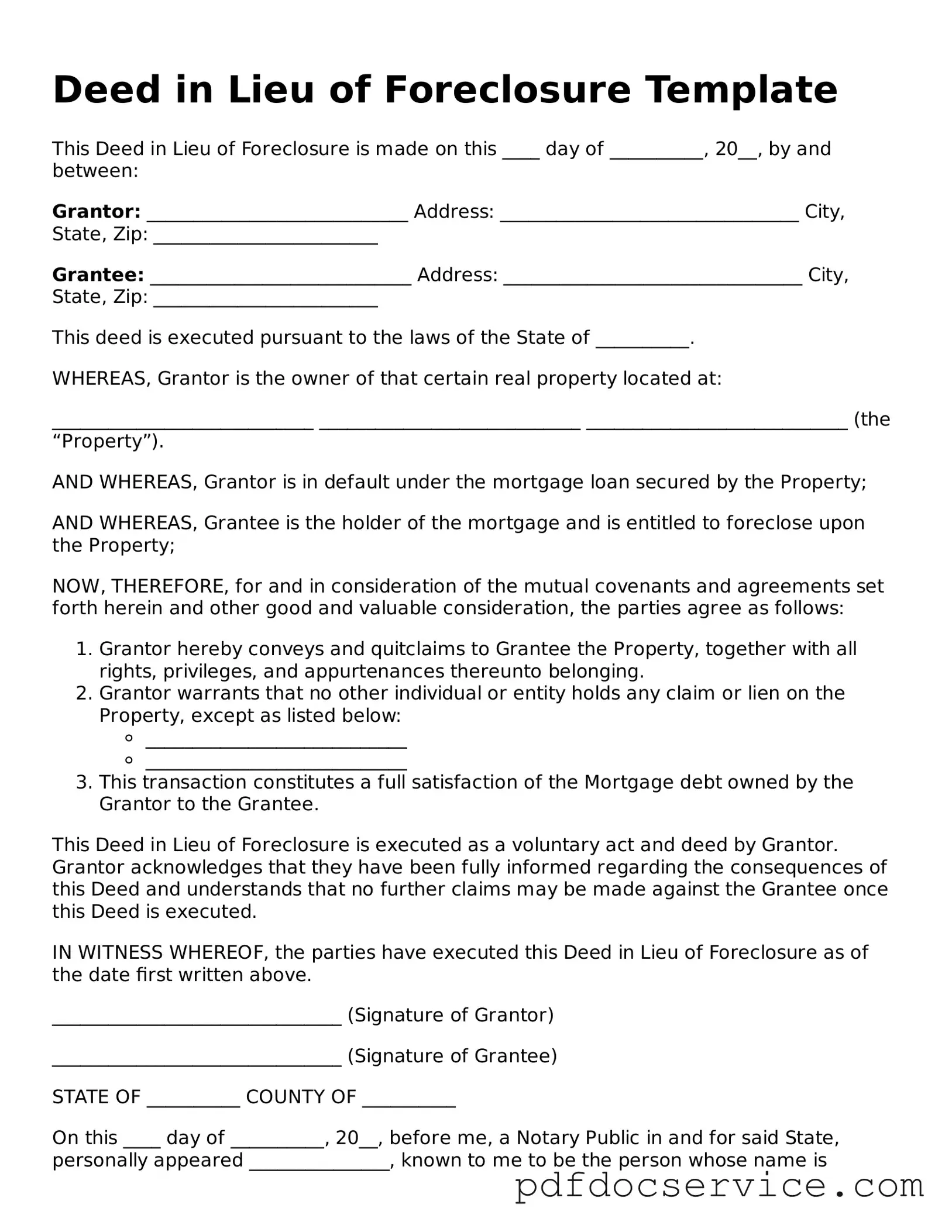

A Deed in Lieu of Foreclosure is a legal document that allows homeowners facing foreclosure to transfer the ownership of their property to the lender. This process can provide a more straightforward and less stressful alternative to the lengthy foreclosure process. By signing this deed, the homeowner relinquishes their rights to the property, and in return, the lender often agrees to forgive the remaining mortgage debt. This agreement can help protect the homeowner's credit score from the more severe impacts of foreclosure. Additionally, it can enable a smoother transition for both parties, as the lender can take possession of the property without going through court proceedings. Understanding the terms and implications of a Deed in Lieu of Foreclosure is essential for homeowners considering this option, as it involves important decisions regarding debt relief and property ownership.

| Fact Name | Details |

|---|---|

| Definition | A Deed in Lieu of Foreclosure is a legal document where a borrower voluntarily transfers ownership of their property to the lender to avoid foreclosure. |

| Purpose | This process helps borrowers avoid the negative consequences of foreclosure, such as damage to credit scores and potential legal actions. |

| Eligibility | Typically, borrowers must be in default on their mortgage payments to qualify for a Deed in Lieu of Foreclosure. |

| State Variations | Each state may have specific forms and requirements. For example, California requires a specific Deed in Lieu of Foreclosure form under California Civil Code Section 2924. |

| Benefits | Borrowers may benefit from a quicker resolution, potential debt forgiveness, and less impact on their credit compared to foreclosure. |

| Risks | Borrowers might still face tax implications on forgiven debt and may lose any rights to contest the foreclosure process. |

| Process | The borrower must negotiate with the lender, complete the necessary paperwork, and may need to provide financial documentation. |

| Legal Advice | It is advisable for borrowers to seek legal counsel before proceeding, as understanding the implications is crucial. |

After completing the Deed in Lieu of Foreclosure form, you will need to submit it to your lender. This action typically begins the process of transferring ownership of the property back to the lender. Make sure to keep copies of all documents for your records.

When considering the Deed in Lieu of Foreclosure, it is essential to understand the implications and processes involved. Here are some key takeaways to guide you through filling out and utilizing this form:

By keeping these takeaways in mind, you can navigate the process of using a Deed in Lieu of Foreclosure with greater confidence and clarity.

Transfer on Death Deed California - This type of deed is often used in estate planning to simplify the transfer of property.

Understanding the importance of a solid contract is key for any buyer or seller. The Texas Tractor Bill of Sale document is vital for ensuring a clear transfer of ownership and protecting both parties involved in the sale. Utilizing this legal form streamlines the transaction process and provides peace of mind for everyone participating in the exchange.

Corrective Deed California - Timeliness in correcting errors is crucial for effective property management.

A Deed in Lieu of Foreclosure is a legal document that allows a homeowner to transfer ownership of their property to the lender to avoid foreclosure. When engaging in this process, several other forms and documents are typically required to ensure clarity and compliance. Below is a list of common documents associated with a Deed in Lieu of Foreclosure.

These documents play a critical role in the Deed in Lieu of Foreclosure process. Each one serves to protect the interests of both the borrower and the lender, ensuring a smooth and legally sound transaction.

A Deed in Lieu of Foreclosure is a legal process that allows a homeowner to voluntarily transfer ownership of their property to the lender in order to avoid foreclosure. This option can be beneficial for both parties, as it may help the homeowner avoid the negative consequences of foreclosure and allow the lender to recover their investment more quickly.

Eligibility for a Deed in Lieu of Foreclosure typically depends on the lender's policies and the homeowner's financial situation. Generally, homeowners who are experiencing financial hardship and are unable to keep up with mortgage payments may qualify. It is important to communicate openly with the lender about your circumstances.

Some benefits include:

Yes, there are some drawbacks to consider. These may include:

The process generally involves the following steps:

In many cases, homeowners may still owe money if the home is worth less than the mortgage balance. However, some lenders may agree to forgive the remaining debt as part of the Deed in Lieu of Foreclosure agreement. It is crucial to clarify this with the lender before proceeding.

Typically, homeowners will need to provide:

Yes, you can still apply for a Deed in Lieu of Foreclosure even if you have missed payments. It is advisable to act as soon as possible, as lenders may be more willing to negotiate when contacted early in the process.

The timeline can vary based on the lender and individual circumstances. Generally, the process may take anywhere from a few weeks to several months. It is essential to maintain open communication with the lender to understand their specific timeline.

If your request is denied, consider the following options: