Printable Deed in Lieu of Foreclosure Template for Florida

Printable Deed in Lieu of Foreclosure Template for Florida

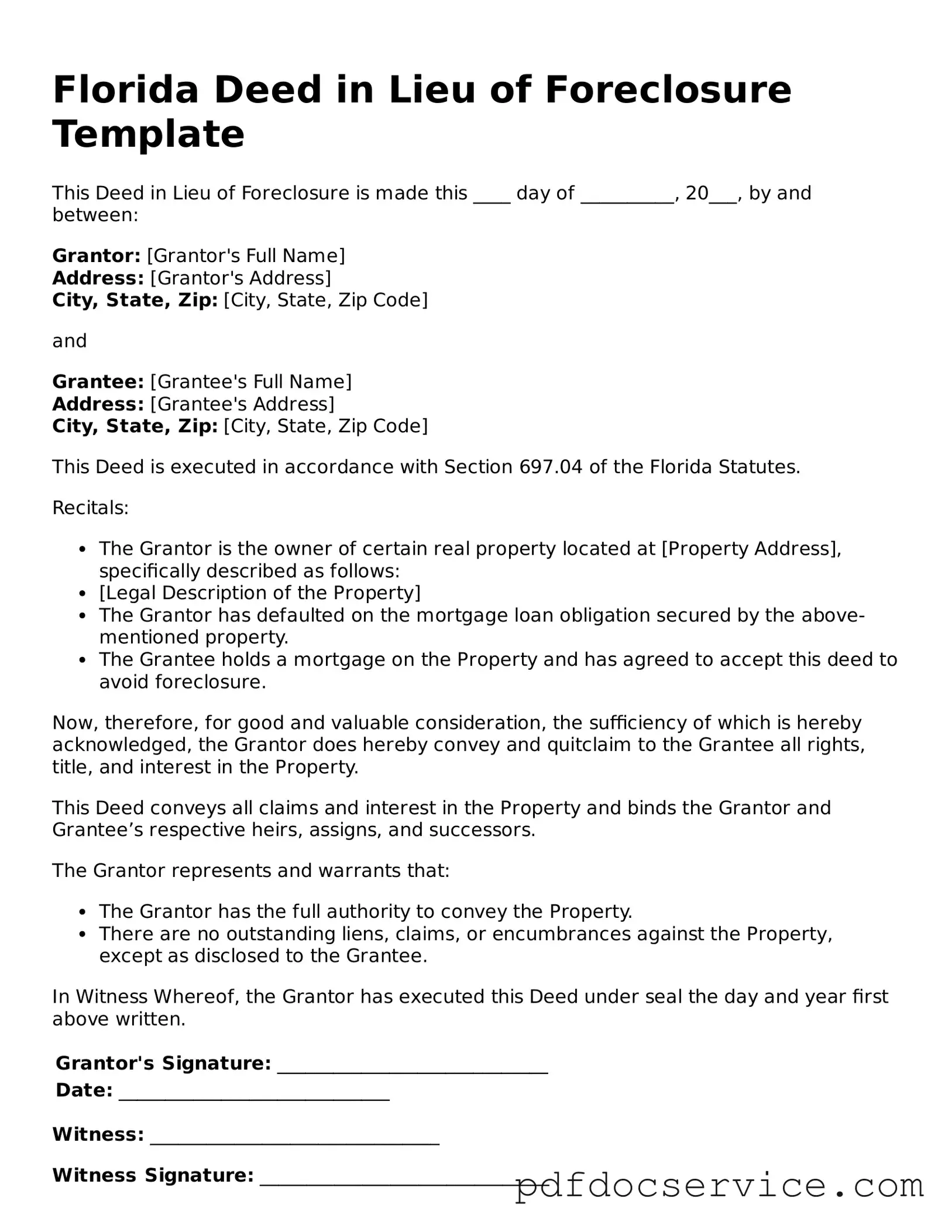

In the state of Florida, homeowners facing financial difficulties may find themselves exploring various options to avoid foreclosure. One such option is the Deed in Lieu of Foreclosure, a legal agreement that allows a borrower to voluntarily transfer ownership of their property to the lender. This process can provide a more streamlined and less stressful alternative to the lengthy foreclosure process. The Deed in Lieu form typically includes essential details such as the property description, the parties involved, and the terms of the transfer. By signing this document, homeowners may be able to mitigate the negative impact on their credit score and potentially negotiate terms that could include the forgiveness of remaining mortgage debt. Understanding the implications of this form is crucial for anyone considering it as a solution to their financial challenges. This article will delve into the intricacies of the Florida Deed in Lieu of Foreclosure form, offering insights into its benefits, potential drawbacks, and the steps involved in the process.

| Fact Name | Description |

|---|---|

| Definition | A Deed in Lieu of Foreclosure is a legal document where a borrower voluntarily transfers property ownership to the lender to avoid foreclosure. |

| Governing Law | In Florida, the process is governed by Chapter 697 of the Florida Statutes. |

| Voluntary Process | This option is voluntary for the borrower, meaning they must agree to the transfer of property. |

| Benefits | A Deed in Lieu can help borrowers avoid the lengthy foreclosure process and its negative impact on credit scores. |

| Property Condition | The property must be in good condition, as lenders may inspect it before accepting the deed. |

| Deficiency Judgments | Borrowers should be aware that lenders may still pursue deficiency judgments, depending on the state laws and the specific terms of the agreement. |

| Alternatives | Other options, such as loan modifications or short sales, may be available and should be considered before choosing a Deed in Lieu. |

Once you have decided to proceed with a Deed in Lieu of Foreclosure, it's important to understand the next steps in the process. Filling out the form accurately is crucial, as it will help facilitate the transfer of property back to the lender. Follow these steps to complete the Florida Deed in Lieu of Foreclosure form correctly.

When considering the Florida Deed in Lieu of Foreclosure form, it is essential to understand several key points. Here are eight important takeaways:

Understanding these points can help homeowners make informed decisions regarding their property and financial situation.

Will I Owe Money After a Deed in Lieu of Foreclosure - This form helps streamline documentation requirements for lenders when accepting property in lieu of foreclosure.

Deed in Lieu of Foreclosure Pa - A Deed in Lieu of Foreclosure allows homeowners to transfer property ownership to the lender to avoid foreclosure.

Completing the NYC Buildings MC-1 form is essential for any proposals aimed at modifying the New York City Electrical Code, allowing for a clear presentation of suggestions and necessary documentation. For those looking for the appropriate templates to facilitate this process, NY PDF Forms can be incredibly helpful in ensuring that all criteria are met efficiently and effectively.

Deed in Lieu of Foreclosure Vs Foreclosure - The deed can improve a borrower's standing in future credit situations, depending on circumstances.

California Property Transfer Deed - The lender usually benefits by receiving the property without the costs associated with foreclosure.

A Deed in Lieu of Foreclosure is a legal instrument that allows a borrower to transfer ownership of their property to the lender in order to avoid the foreclosure process. This document is often accompanied by several other forms and documents that help facilitate the transfer and protect the interests of both parties. Below is a list of these commonly used documents.

In summary, these documents play a crucial role in the Deed in Lieu of Foreclosure process. They help clarify the responsibilities and rights of both the borrower and the lender, ensuring a smoother transition of property ownership while minimizing potential disputes.

A Deed in Lieu of Foreclosure is a legal process where a homeowner voluntarily transfers the title of their property to the lender to avoid foreclosure. This option allows the borrower to relinquish ownership of the property, thus settling the mortgage debt without going through the lengthy and often costly foreclosure process.

Eligibility typically includes homeowners who are facing financial difficulties and are unable to continue making mortgage payments. Lenders generally require that the homeowner has exhausted all other options, such as loan modifications or short sales, before considering a Deed in Lieu of Foreclosure. Additionally, the property must be free of any other liens that could complicate the transfer.

Several benefits exist for homeowners who choose this option, including:

While there are benefits, some drawbacks include:

The process generally involves several steps:

In many cases, homeowners may be released from their mortgage obligation after a Deed in Lieu of Foreclosure. However, this is not guaranteed. It is essential to clarify this aspect with the lender before proceeding, as some lenders may require the borrower to sign a deficiency waiver to ensure no further debt remains.

A Deed in Lieu of Foreclosure can still negatively impact a homeowner's credit score, but typically less severely than a full foreclosure. The exact impact depends on various factors, including the homeowner's credit history and the lender's reporting practices. It is advisable to check with credit reporting agencies to understand the potential effects.

Yes, negotiation is often a part of the process. Homeowners can discuss various terms, including the potential for debt forgiveness and the timeline for vacating the property. Open communication with the lender can lead to a more favorable outcome.

If you are considering this option, it is crucial to:

Yes, several alternatives exist, including:

Each option has its own set of pros and cons, so it is essential to evaluate them carefully.