Printable Loan Agreement Template for Florida

Printable Loan Agreement Template for Florida

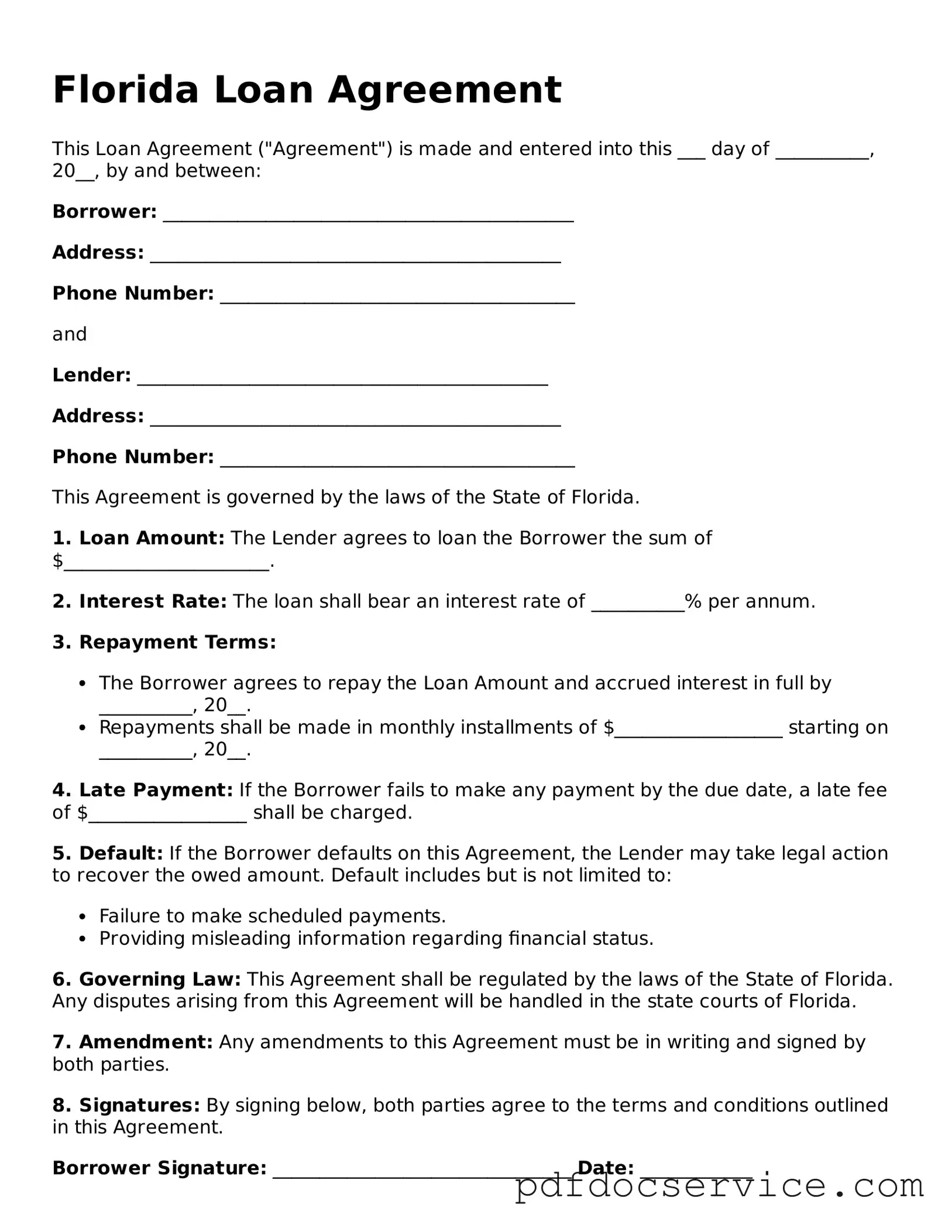

The Florida Loan Agreement form serves as a crucial document for individuals and businesses engaged in lending and borrowing transactions within the state. This form outlines the specific terms and conditions under which a loan is granted, ensuring that both parties have a clear understanding of their rights and obligations. Key components typically include the loan amount, interest rate, repayment schedule, and any collateral that may be required to secure the loan. Additionally, the agreement may address late fees, default terms, and other important clauses that protect the interests of both the lender and the borrower. By clearly detailing these aspects, the Loan Agreement helps to minimize misunderstandings and disputes that could arise during the life of the loan. Utilizing this form not only formalizes the lending process but also provides a legal framework that can be referred to in case of disagreements, making it an essential tool for anyone involved in financial transactions in Florida.

Promissory Note: This document outlines the borrower's promise to repay a specific amount of money to the lender, similar to a loan agreement in that it details the terms of repayment.

Mortgage Agreement: This document secures a loan with real property, ensuring that the lender has a claim against the property if the borrower defaults, much like a loan agreement establishes the terms for borrowing.

Security Agreement: This document provides collateral for a loan, detailing the assets pledged by the borrower, similar to how a loan agreement specifies the conditions of the loan.

Credit Agreement: This outlines the terms under which a borrower can access credit, mirroring the loan agreement's focus on repayment terms and conditions.

Personal Guarantee: This document holds an individual responsible for the loan, similar to how a loan agreement holds the borrower accountable for repayment.

Lease Agreement: While primarily for renting property, it shares similarities in outlining obligations and terms between parties, akin to the structure of a loan agreement.

Installment Agreement: This document allows for the repayment of debts in installments, paralleling the payment structure often found in loan agreements.

Partnership Agreement: This document outlines the terms of a partnership, including financial contributions, similar to how a loan agreement details the financial obligations of the borrower.

Debt Settlement Agreement: This outlines the terms under which a debtor agrees to pay a reduced amount, similar in purpose to a loan agreement but focused on resolving existing debt.

| Fact Name | Description |

|---|---|

| Purpose | The Florida Loan Agreement form is used to outline the terms and conditions of a loan between a lender and a borrower. |

| Governing Law | The agreement is governed by the laws of the State of Florida. |

| Loan Amount | The form specifies the total amount of money being loaned to the borrower. |

| Interest Rate | The agreement includes the interest rate that will be applied to the loan amount. |

| Repayment Terms | It outlines the schedule for repayment, including due dates and payment amounts. |

| Default Conditions | The form details the conditions under which the borrower may be considered in default of the loan. |

| Signatures | Both the lender and borrower must sign the agreement to make it legally binding. |

| Amendments | The agreement may include provisions for amendments, which must also be documented in writing. |

Filling out the Florida Loan Agreement form is an important step in formalizing a loan arrangement. By following the steps outlined below, you will ensure that all necessary information is accurately provided, which will help in creating a clear and binding agreement between the parties involved.

Once the form is filled out and signed, it is advisable to keep a copy in a safe place. This will serve as a reference for both parties should any questions or issues arise in the future.

When navigating the Florida Loan Agreement form, it's essential to understand its components and implications. Here are some key takeaways to consider:

By keeping these key points in mind, individuals can effectively fill out and utilize the Florida Loan Agreement form, fostering a transparent and legally sound lending process.

Promissory Note New York - An amendment section might detail how changes to the agreement can be made.

To ensure a smooth transaction when purchasing or selling agricultural equipment, it is advisable to use a reliable document such as the "Texas Tractor Bill of Sale" that outlines all necessary details. This document serves as a crucial legal record. For a user-friendly template, check out this comprehensive Texas Tractor Bill of Sale document.

Texas Promissory Note Template - This document can ensure that the lender's interests are safeguarded.

Sample Promissory Note California - A Loan Agreement can be tailored to fit individual needs.

Maryland Promissory Note - Includes terms related to governing law that will apply to the agreement.

When entering into a loan agreement in Florida, several additional forms and documents may be necessary to ensure clarity and legal compliance. Each of these documents serves a specific purpose and helps protect the interests of both the lender and the borrower.

Understanding these documents can help borrowers and lenders navigate the loan process more effectively. Each form plays a crucial role in establishing clear expectations and protecting the rights of all parties involved.

A Florida Loan Agreement is a legal document that outlines the terms and conditions of a loan between a lender and a borrower. It specifies the amount borrowed, interest rates, repayment terms, and any collateral involved. This agreement serves to protect both parties by clearly defining their rights and responsibilities.

Any individual or business in Florida seeking to lend or borrow money can use this agreement. It is commonly utilized by private lenders, banks, and individuals who want to formalize a loan arrangement. Both parties should ensure they understand the terms before signing.

A comprehensive Florida Loan Agreement typically includes the following components:

While it is not legally required to have a lawyer review the Loan Agreement, it is highly recommended. A legal professional can ensure that the terms are fair and comply with Florida laws. This review can help prevent misunderstandings and disputes in the future.

If the borrower defaults, the lender has several options, which may include:

The specific actions available will depend on the terms outlined in the Loan Agreement.

Yes, a Florida Loan Agreement can be modified after it is signed, but both parties must agree to the changes. It is advisable to document any modifications in writing and have both parties sign the amended agreement to ensure clarity and enforceability.

Florida Loan Agreement forms can be obtained from various sources, including:

When selecting a form, ensure it is up-to-date and complies with Florida laws.