Printable Promissory Note Template for Florida

Printable Promissory Note Template for Florida

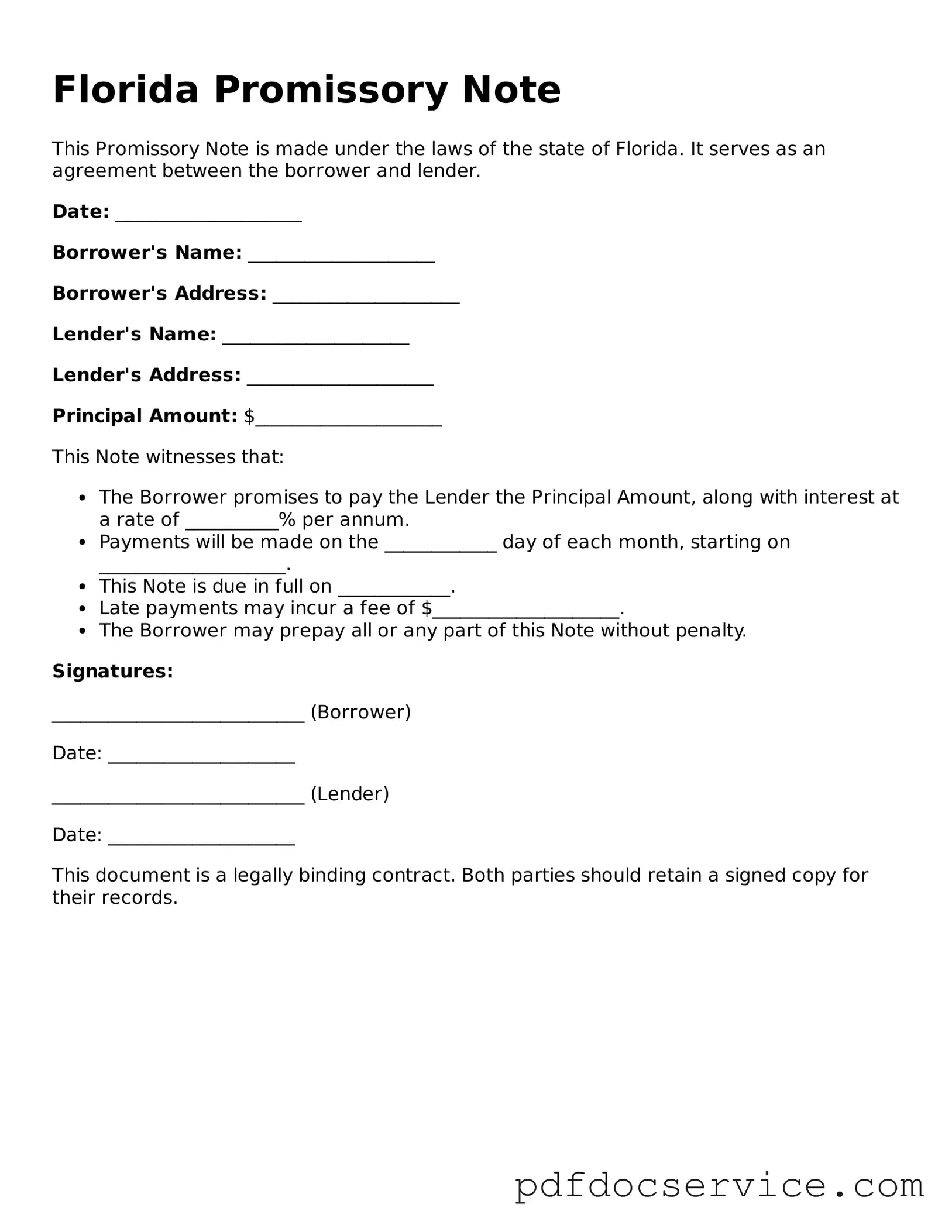

In Florida, a Promissory Note serves as a vital financial instrument that outlines the terms of a loan between a lender and a borrower. This legally binding document details the amount borrowed, the interest rate, and the repayment schedule, ensuring clarity and accountability for both parties involved. It typically includes provisions for late fees, default consequences, and the option for prepayment, which protects the lender's interests while providing flexibility for the borrower. By specifying the conditions under which the loan must be repaid, the Promissory Note helps to prevent misunderstandings and disputes. Understanding the key elements of this form is essential for anyone looking to engage in lending or borrowing in Florida, as it lays the groundwork for a transparent financial relationship.

| Fact Name | Description |

|---|---|

| Definition | A Florida Promissory Note is a written promise to pay a specified amount of money to a lender at a defined time. |

| Governing Law | Florida Statutes, Chapter 673 governs promissory notes in Florida. |

| Parties Involved | The note involves two parties: the borrower (maker) and the lender (payee). |

| Interest Rate | The interest rate can be fixed or variable, as agreed upon by both parties. |

| Payment Terms | Payment terms must be clearly outlined, including the due date and method of payment. |

| Enforceability | A properly executed promissory note is legally enforceable in Florida courts. |

Once you have the Florida Promissory Note form in hand, you are ready to begin the process of filling it out. This form is crucial for documenting a loan agreement between a lender and a borrower. Ensuring that all sections are completed accurately will help in avoiding misunderstandings in the future.

After completing the form, it is advisable to keep copies for both parties. This ensures that everyone has a record of the agreement. If any changes are made after signing, those should be documented properly to avoid any future disputes.

When it comes to using a Florida Promissory Note form, there are several important points to keep in mind. Understanding these key aspects can help ensure that the document serves its intended purpose effectively.

By keeping these takeaways in mind, you can navigate the process of filling out and using a Florida Promissory Note more effectively.

North Dakota Money Promissory Note - Some promissory notes incorporate clauses for mediation in case of disputes between parties.

Tennessee Promissory Note - A promissory note can strengthen trust and accountability between lender and borrower.

Promissory Note Template California - Both parties should understand their rights and obligations as outlined in the note.

The New York Operating Agreement form not only serves as a vital document for limited liability companies (LLCs) in New York, but it also ensures that members are well-informed about their roles and responsibilities. To create a comprehensive agreement that helps prevent disputes and protects the interests of all members involved, it can be beneficial to refer to resources like mypdfform.com/blank-new-york-operating-agreement.

Online Promissory Note - Borrowers should keep copies of the note for their records.

When dealing with a Florida Promissory Note, there are several other documents that are often used in conjunction to ensure clarity and legal protection for all parties involved. Understanding these forms can help you navigate the lending process more smoothly.

Each of these documents plays a crucial role in the lending process, providing clarity and protection for both the lender and borrower. By being familiar with these forms, you can ensure that all aspects of your financial agreement are well-documented and understood.

A Florida Promissory Note is a written promise to pay a specific amount of money to a designated person or entity at a specified time. It outlines the terms of the loan, including the interest rate, repayment schedule, and any penalties for late payments. This document serves as a legal record of the agreement between the borrower and the lender.

Anyone can use a Florida Promissory Note, whether they are individuals, businesses, or organizations. It is commonly used in personal loans, business loans, and real estate transactions. Both the borrower and lender should understand the terms before signing the document to ensure clarity and agreement on the loan conditions.

A typical Florida Promissory Note includes several important components:

If a borrower fails to repay the loan as agreed, the lender can take legal action to enforce the Promissory Note. This might involve filing a lawsuit to recover the owed amount. The note serves as evidence of the debt, making it easier for the lender to prove their case in court. It's important for both parties to keep a copy of the signed note for their records.