Fill Your IRS Schedule C 1040 Form

Fill Your IRS Schedule C 1040 Form

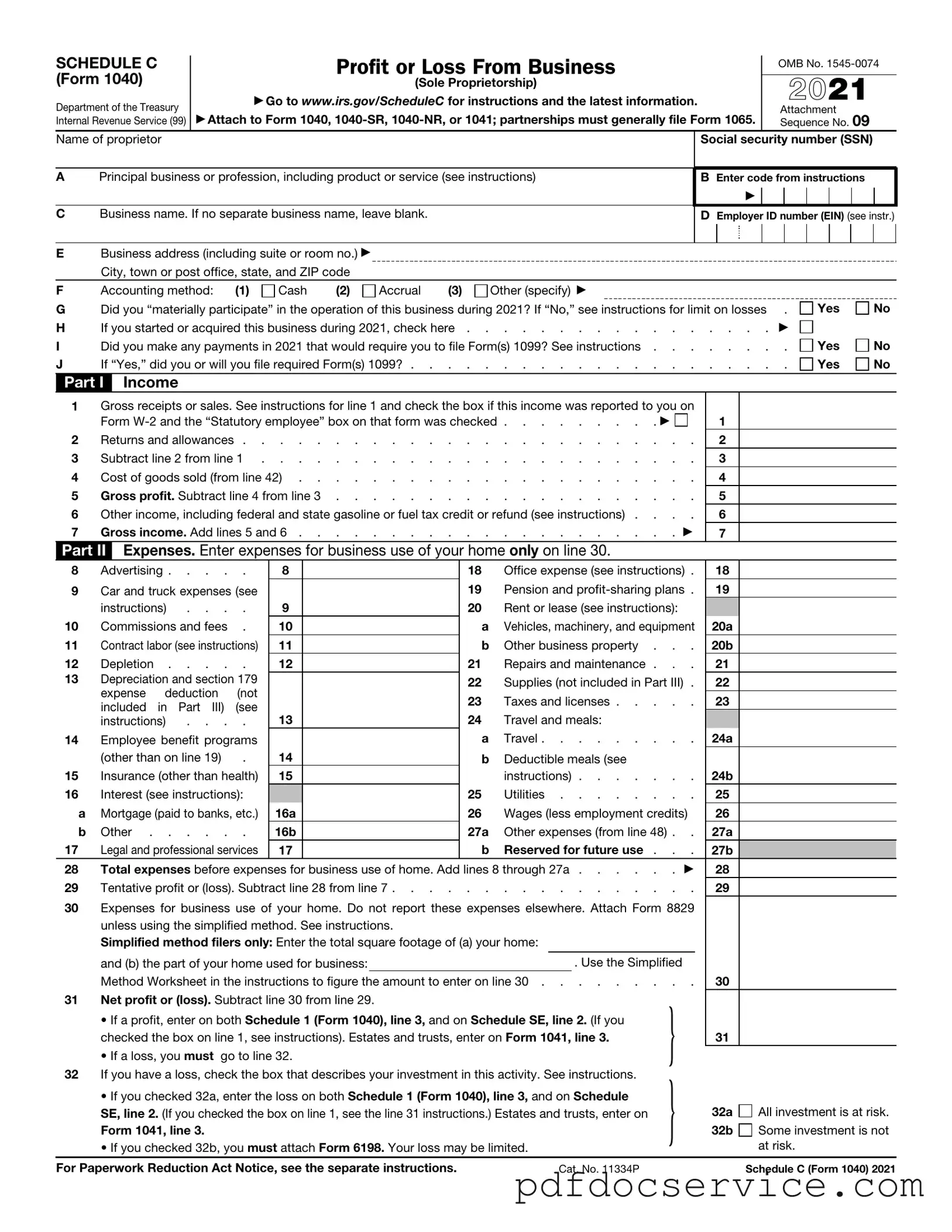

For many individuals running their own businesses or engaging in self-employment, understanding the IRS Schedule C (Form 1040) is essential for accurate tax reporting. This form allows sole proprietors to report income or loss from their business activities, providing a comprehensive overview of earnings, expenses, and net profit or loss. It captures a variety of important details, such as the type of business, gross receipts, and specific deductions that can significantly impact taxable income. Common expenses reported on Schedule C include costs related to advertising, supplies, and vehicle use, among others. Additionally, the form requires careful attention to ensure compliance with IRS regulations, making it crucial for taxpayers to keep detailed records throughout the year. Filing Schedule C correctly not only helps in calculating taxes owed but also plays a vital role in establishing the financial health of a business. Understanding its components and requirements can empower self-employed individuals to navigate their tax obligations with confidence.

Form 1065: This form is used by partnerships to report income, deductions, and profits. Similar to Schedule C, it provides a detailed breakdown of business earnings and expenses, helping the IRS understand the financial situation of the business entity.

Non-compete Agreement: This legal document protects employers by restricting employees from competing against them during and after employment. For more information, you can refer to NY PDF Forms.

Form 1120: Corporations file this form to report their income, gains, losses, deductions, and credits. Like Schedule C, it serves to outline the financial activities of a business, but it is specifically for corporations rather than sole proprietorships.

Form 1120S: This is the tax return for S corporations. It shares similarities with Schedule C in that it details income and expenses, but it is tailored for S corporations, which pass their income directly to shareholders.

Schedule E: Used for reporting supplemental income and loss, such as rental income or royalties. Schedule E, like Schedule C, requires detailed reporting of income and expenses, but it focuses on passive income rather than active business operations.

Form 990: Nonprofit organizations use this form to report their financial information. While Schedule C focuses on profit-making businesses, both forms require transparency about income and expenses to ensure compliance with tax regulations.

Form 1040: This is the individual income tax return form. Schedule C is attached to Form 1040 for sole proprietors, as it details business income and expenses that contribute to the individual's overall tax liability.

Schedule F: Farmers use this schedule to report farm income and expenses. Similar to Schedule C, it requires detailed documentation of earnings and costs, tailored specifically for agricultural businesses.

| Fact Name | Description |

|---|---|

| Purpose | The IRS Schedule C (Form 1040) is used by sole proprietors to report income or loss from their business. |

| Filing Requirement | Individuals must file Schedule C if they have earned income from self-employment and their net earnings exceed $400. |

| Deductions | Business expenses such as supplies, equipment, and travel can be deducted to reduce taxable income. |

| State-Specific Forms | Some states may require additional forms for business income reporting. For example, California uses Form 540 for personal income tax, which includes business income reporting under state law. |

Filling out the IRS Schedule C (Form 1040) is an essential step for self-employed individuals or those running a business as a sole proprietor. This form allows you to report income, expenses, and profits from your business activities. Completing it accurately is crucial for your tax return and can help you understand your business's financial health.

Once you have filled out the Schedule C form, you can proceed to file your complete tax return. Ensure you keep a copy of your Schedule C and all supporting documents for your records, as you may need them in the future for audits or other inquiries.

When filling out and using the IRS Schedule C (Form 1040), there are several important points to consider. Understanding these can help ensure compliance and accuracy in reporting income from self-employment.

By keeping these key takeaways in mind, you can navigate the process of completing Schedule C more effectively and minimize potential issues with the IRS.

5 Year Workmanship Warranty Roofing - We stand behind our work with a robust warranty for homeowners.

Creating a comprehensive Last Will and Testament is vital for safeguarding your wishes and ensuring your loved ones are supported after your passing. For those looking to draft this important document, you can find a useful resource at mypdfform.com/blank-last-will-and-testament/, where you can access a blank form to start outlining your desires regarding asset distribution and family care.

Car Repair Estimate Template - List any previous repairs related to the current issues.

The IRS Schedule C (Form 1040) is used by sole proprietors to report income and expenses from their business. When filing this form, several other documents may be necessary to provide a complete picture of the taxpayer's financial situation. Below are five common forms and documents that often accompany Schedule C.

These documents collectively assist in accurately reporting income and expenses, ensuring compliance with IRS regulations. Proper preparation and organization of these forms can facilitate a smoother tax filing process.

IRS Schedule C is a form used by sole proprietors to report income or loss from their business. If you operate a business as a sole proprietor or are a single-member LLC, you will likely need to file this form along with your personal income tax return (Form 1040). It's essential for reporting earnings, expenses, and determining your net profit or loss for the year.

When completing Schedule C, you should report all income generated from your business activities. This includes:

It's crucial to keep accurate records of all income sources to ensure compliance and maximize potential deductions.

Deducting business expenses can significantly reduce your taxable income. Common deductible expenses include:

Always keep receipts and documentation for these expenses, as they may be required for verification during an audit.

To calculate your net profit or loss, start by adding all your business income. Then, subtract your total business expenses from this income. The formula looks like this:

Net Profit or Loss = Total Income - Total Expenses

If the result is positive, you have a net profit, which will be taxable. If it's negative, you have a net loss, which may offset other income on your tax return. Understanding this calculation is vital for managing your tax obligations effectively.