Blank Letter of Intent to Purchase Business Form

Blank Letter of Intent to Purchase Business Form

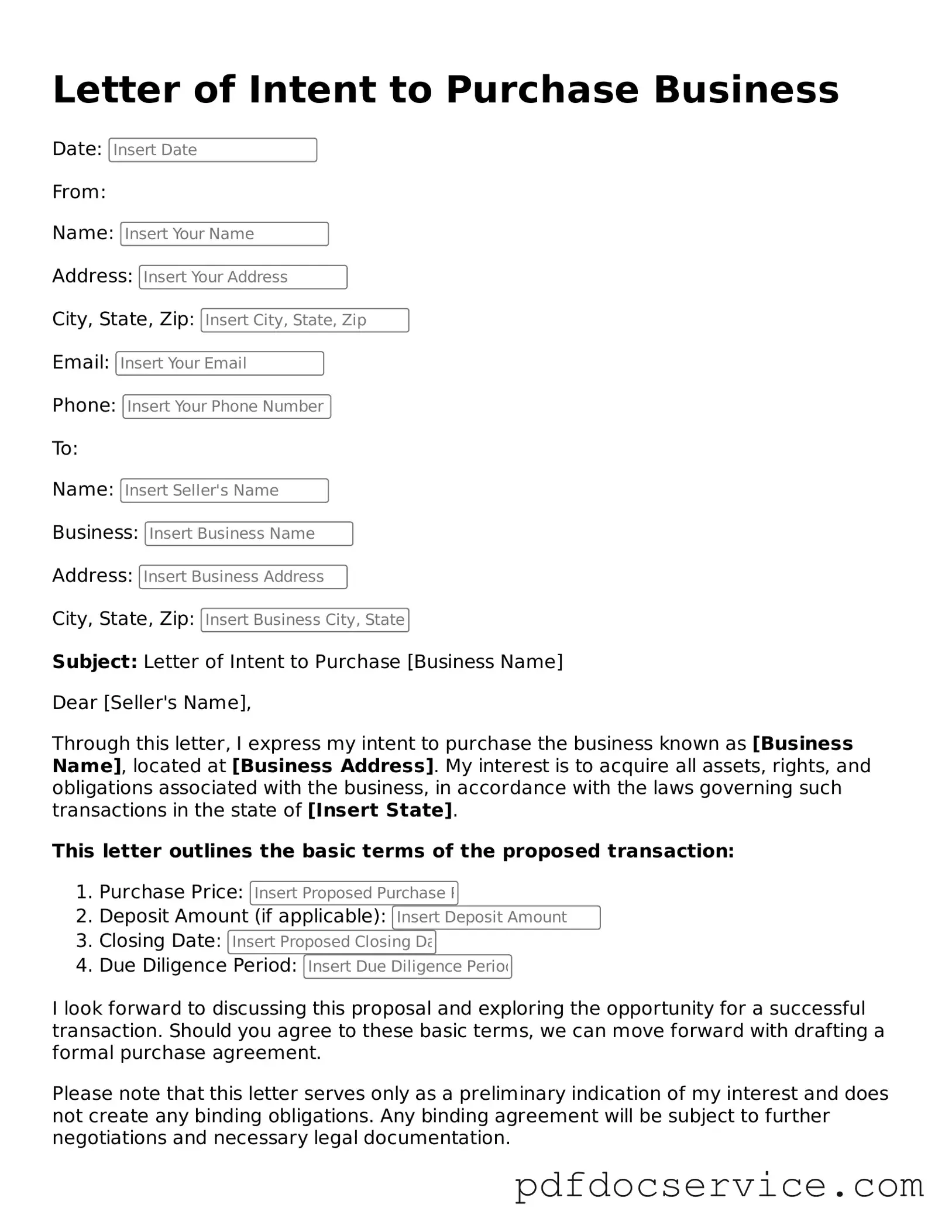

When considering the purchase of a business, one of the first important steps is to draft a Letter of Intent (LOI) to Purchase Business. This document serves as a preliminary agreement between the buyer and the seller, outlining the key terms and conditions that will guide the eventual sale. It typically includes essential elements such as the purchase price, payment terms, and any contingencies that may need to be addressed before the final agreement is reached. Additionally, the LOI often specifies the timeline for due diligence, allowing both parties to gather necessary information and assess the viability of the transaction. While this letter is not legally binding in most cases, it establishes a framework for negotiation and demonstrates the buyer's serious intent to move forward. By clearly communicating expectations and responsibilities, the Letter of Intent can help prevent misunderstandings and pave the way for a smoother transaction process. Understanding the nuances of this form can significantly impact the overall success of the business acquisition journey.

| Fact Name | Description |

|---|---|

| Purpose | A Letter of Intent (LOI) outlines the preliminary agreement between a buyer and seller regarding the purchase of a business. |

| Non-Binding Nature | Typically, an LOI is non-binding, meaning that it does not create a legal obligation to complete the transaction. |

| Key Components | Common elements include purchase price, payment terms, and timelines for due diligence and closing. |

| Confidentiality Clause | Many LOIs include a confidentiality clause to protect sensitive information shared during negotiations. |

| State-Specific Forms | Some states may have specific requirements or forms for LOIs, governed by local commercial laws. |

| Governing Law | The LOI may specify the governing law, which is the state law that will apply in case of disputes. |

Filling out a Letter of Intent to Purchase a Business is an important step in the buying process. This document outlines your intentions and can help set the stage for negotiations. After completing the form, you’ll be ready to discuss terms with the seller and move forward with the transaction.

Once you have completed the form, review it for accuracy. Make copies for your records and send it to the seller. This will initiate discussions and help both parties understand the next steps in the purchasing process.

Filling out a Letter of Intent (LOI) to Purchase a Business is a crucial step in the acquisition process. Here are five key takeaways to consider when completing this form:

By keeping these key points in mind, you can effectively navigate the process of filling out and using a Letter of Intent to Purchase a Business.

What Is Letter of Intent for Job - Marks an important step in the employment process.

Completing the Kentucky Homeschool Letter of Intent is an essential task for parents or guardians looking to begin their homeschooling journey, as it acts as a formal notification to the local school district. By submitting this crucial document, families can ensure they are compliant with state regulations, which facilitates a smoother transition into homeschooling. For more detailed guidance on this process, you can refer to the Homeschool Letter of Intent, which outlines the necessary steps and considerations.

A Letter of Intent to Purchase Business is often just the beginning of a detailed process. Several other forms and documents are typically needed to ensure a smooth transaction. Below is a list of these important documents, each serving a specific purpose in the purchase process.

Each of these documents plays a crucial role in the business acquisition process. They help protect the interests of both the buyer and the seller, ensuring a clear understanding of the transaction. Properly preparing and reviewing these documents can lead to a successful business purchase.

A Letter of Intent (LOI) to purchase a business is a preliminary document that outlines the intentions of a buyer to acquire a business. It serves as a starting point for negotiations and can help clarify the terms and conditions under which the buyer is willing to proceed. While it is not a legally binding contract, it often includes important details that both parties agree to in principle.

The LOI is important for several reasons. First, it helps establish a mutual understanding between the buyer and the seller regarding the basic terms of the sale. This can include the purchase price, payment structure, and timeline. Additionally, it can provide a framework for due diligence, ensuring that both parties are on the same page before committing to a formal purchase agreement.

Typically, an LOI should include the following elements:

Generally, a Letter of Intent is not legally binding, meaning that it does not create a legal obligation for either party to complete the transaction. However, certain provisions within the LOI, such as confidentiality agreements or exclusivity clauses, can be binding. It is crucial for both parties to understand which parts of the LOI are enforceable and which are not.

A Letter of Intent is a preliminary document that outlines the basic terms of a potential sale, while a purchase agreement is a formal, legally binding contract that finalizes the terms of the transaction. The purchase agreement will include more detailed provisions, including representations, warranties, and conditions that must be met before the sale can be completed.

An LOI is typically used early in the negotiation process, after initial discussions have taken place but before a formal purchase agreement is drafted. It is particularly useful when both parties want to ensure that they are aligned on key terms before investing time and resources into due diligence and contract drafting.

Yes, a Letter of Intent can be modified after it is signed, provided that both parties agree to the changes. It is advisable to document any modifications in writing to avoid misunderstandings later in the process. Clear communication is essential to ensure that all parties are aware of and agree to the changes made.

Some risks associated with using a Letter of Intent include:

To ensure that a Letter of Intent is effective, consider the following best practices: