Blank Loan Agreement Form

Blank Loan Agreement Form

When individuals or businesses seek financial assistance, a Loan Agreement form becomes an essential tool in defining the terms of the borrowing arrangement. This document outlines critical components such as the loan amount, interest rate, repayment schedule, and any collateral involved. By clearly detailing the obligations of both the lender and borrower, the agreement serves to protect the interests of both parties while establishing a clear framework for the transaction. It also addresses potential scenarios such as default and the remedies available to the lender, ensuring that all parties understand the consequences of non-compliance. Additionally, the Loan Agreement form may include provisions for prepayment options and late fees, offering flexibility and clarity in the borrowing process. Overall, this form not only facilitates trust between the lender and borrower but also helps to prevent misunderstandings that could lead to disputes down the line.

Promissory Note: Like a Loan Agreement, a Promissory Note outlines the terms of a loan, including the amount borrowed and the repayment schedule. However, it is typically a simpler document and may not include detailed terms about collateral or conditions.

Mortgage Agreement: This document secures a loan with real property. Similar to a Loan Agreement, it details the loan amount and terms, but it also specifies the property being used as collateral.

Lease Agreement: While primarily used for renting property, a Lease Agreement can have similar elements to a Loan Agreement, such as payment terms and duration. Both documents establish a financial obligation between parties.

Security Agreement: This document is used to create a security interest in personal property. Like a Loan Agreement, it outlines the terms of the loan but focuses on the collateral that secures the loan.

Credit Agreement: A Credit Agreement is similar in that it outlines the terms under which credit is extended, including interest rates and repayment terms, much like a Loan Agreement does.

Loan Modification Agreement: This document modifies the terms of an existing Loan Agreement. It retains many of the original elements but changes specifics like interest rates or repayment schedules.

Personal Guarantee: A Personal Guarantee can accompany a Loan Agreement, ensuring that an individual will repay the loan if the borrower defaults. It shares the financial obligation aspect of the Loan Agreement.

Installment Sale Agreement: This document outlines a sale where payments are made over time. Like a Loan Agreement, it specifies payment terms and can involve interest on the outstanding balance.

Partnership Agreement: While primarily focused on business relationships, it can include provisions for loans between partners. It shares the financial agreement aspect found in Loan Agreements.

Business Loan Agreement: Specifically for business loans, this document includes terms similar to a Loan Agreement but is tailored for business needs, including repayment terms and conditions related to business operations.

| Fact Name | Details |

|---|---|

| Definition | A Loan Agreement is a contract between a lender and a borrower outlining the terms of a loan. |

| Parties Involved | The agreement includes the lender, who provides the funds, and the borrower, who receives the funds. |

| Loan Amount | The specific amount of money being borrowed is clearly stated in the agreement. |

| Interest Rate | The agreement specifies the interest rate applied to the loan, which can be fixed or variable. |

| Repayment Terms | Details about how and when the loan will be repaid are outlined, including payment frequency. |

| Governing Law | The agreement is governed by the laws of the state where it is executed, which can vary by state. |

| Default Clause | The agreement includes terms that define what constitutes a default and the consequences thereof. |

| Signatures | Both parties must sign the agreement to make it legally binding, often requiring witnesses or notarization. |

Once you have the Loan Agreement form in hand, it’s important to complete it accurately to ensure that all necessary information is provided. This will help facilitate the processing of your loan request. Follow the steps below to fill out the form correctly.

After completing the form, you will need to submit it to the appropriate party for review. Make sure to follow any additional instructions provided by the lender to ensure a smooth process.

When filling out and using a Loan Agreement form, it's essential to keep several key points in mind. Here are nine important takeaways to consider:

By following these guidelines, both borrowers and lenders can ensure a smoother transaction and a clearer understanding of their obligations.

Bill of Sale for 4 Wheeler - Providing accurate details leads to a smoother transaction experience.

Drawer Count Sheet - Enhance operational efficiency by implementing this form regularly.

A Loan Agreement form is often accompanied by several other documents that provide additional information or support the terms of the loan. Below is a list of commonly used forms and documents associated with a Loan Agreement.

These documents collectively help ensure that both the lender and borrower have a clear understanding of the loan terms and obligations. Proper documentation is essential for protecting the interests of all parties involved.

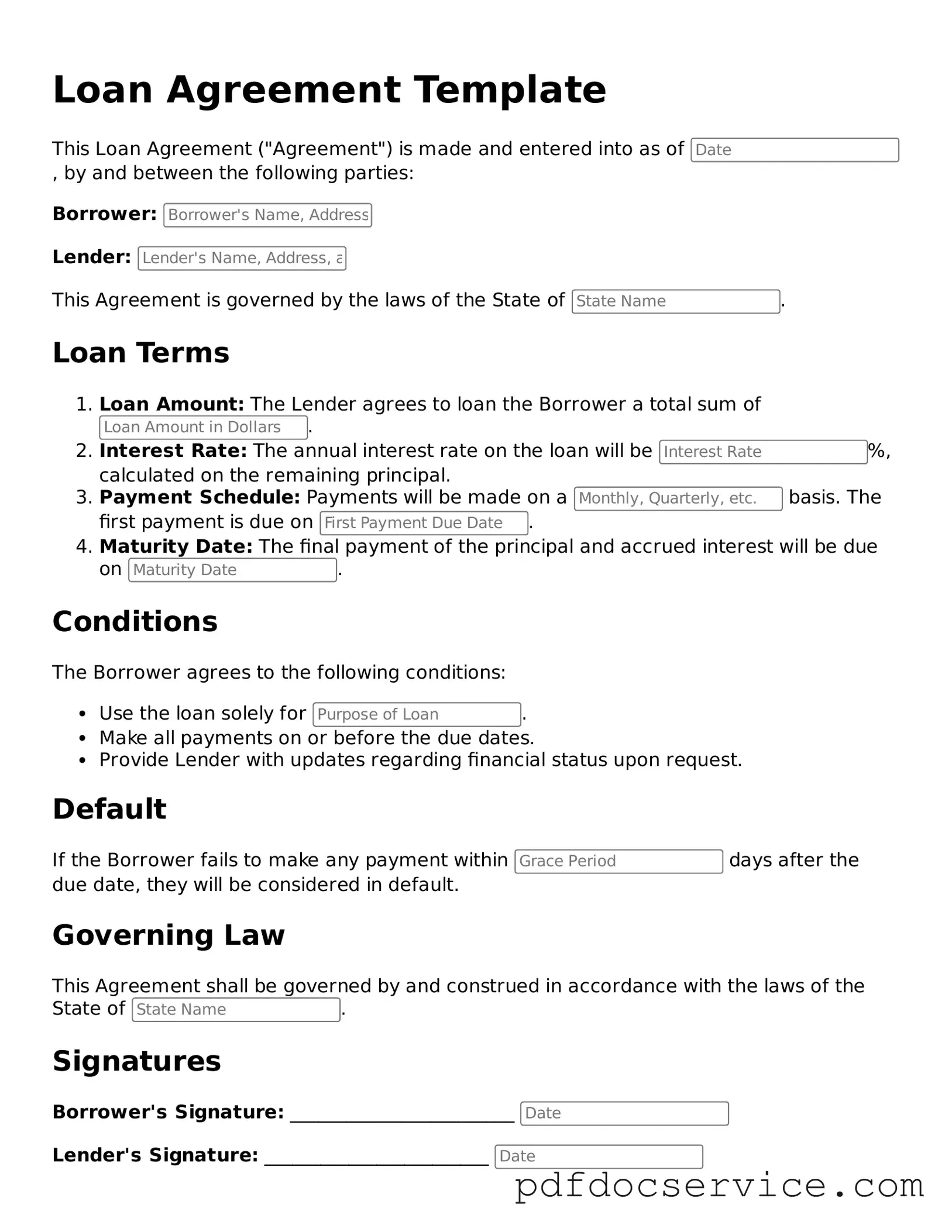

A Loan Agreement form is a legal document that outlines the terms and conditions under which a borrower receives funds from a lender. This agreement serves as a binding contract, detailing the obligations of both parties. It typically includes information such as the loan amount, interest rate, repayment schedule, and any collateral involved. By signing this document, both the lender and borrower acknowledge their understanding and acceptance of the terms outlined within it.

Having a Loan Agreement is crucial for several reasons:

A comprehensive Loan Agreement should contain the following elements:

Yes, a Loan Agreement can be modified after it is signed, but both parties must agree to the changes. It is advisable to document any amendments in writing, ensuring that both the lender and borrower sign the revised agreement. This helps maintain clarity and provides a record of the new terms. Verbal agreements or informal modifications may lead to confusion and potential disputes, so a formal approach is always recommended.

If a borrower defaults on the Loan Agreement, the lender has several options. Typically, the lender may:

It is essential for both parties to communicate openly and seek resolution before escalating the situation, as maintaining a good relationship can often lead to mutually beneficial solutions.