Printable Deed in Lieu of Foreclosure Template for New York

Printable Deed in Lieu of Foreclosure Template for New York

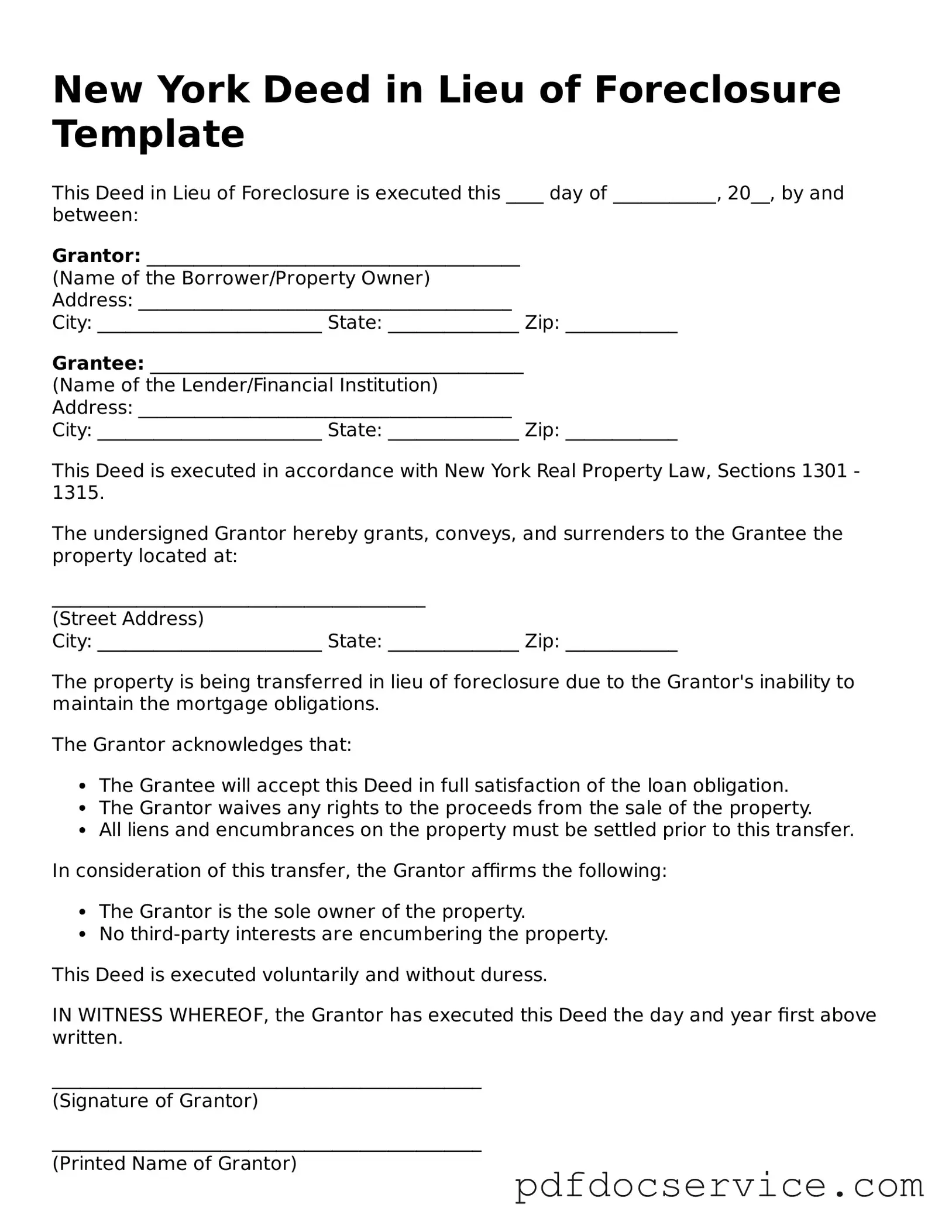

In the realm of real estate, navigating financial difficulties can be daunting for homeowners facing foreclosure. One potential solution that may ease this burden is the New York Deed in Lieu of Foreclosure form. This legal instrument allows a borrower to voluntarily transfer their property title back to the lender, effectively satisfying the mortgage obligation without undergoing the lengthy foreclosure process. The form typically includes essential details such as the property description, the names of the parties involved, and any outstanding debts associated with the mortgage. By utilizing this form, homeowners can mitigate the negative impact on their credit score, as it may be viewed more favorably than a foreclosure. Additionally, lenders often prefer this option, as it saves them time and resources while allowing them to recover their investment more efficiently. Understanding the nuances of this form is crucial for homeowners considering it as a viable alternative to foreclosure.

A Deed in Lieu of Foreclosure is a legal document that allows a homeowner to transfer ownership of their property to the lender to avoid foreclosure. This form has similarities with several other documents in the realm of real estate and finance. Here’s a list of nine documents that share characteristics with the Deed in Lieu of Foreclosure:

Understanding these documents can help homeowners explore their options when facing financial difficulties and seeking to avoid foreclosure.

| Fact Name | Description |

|---|---|

| Definition | A deed in lieu of foreclosure is a legal document where a borrower voluntarily transfers the title of their property to the lender to avoid foreclosure proceedings. |

| Governing Law | In New York, the deed in lieu of foreclosure is governed by New York Real Property Actions and Proceedings Law (RPAPL). |

| Benefits | This process can help borrowers avoid the lengthy and costly foreclosure process, and it may have a less negative impact on their credit score. |

| Considerations | Borrowers should be aware that lenders may require a full financial disclosure and may still pursue a deficiency judgment if the property value is less than the outstanding mortgage balance. |

Once you have decided to proceed with a Deed in Lieu of Foreclosure in New York, filling out the form correctly is crucial. This process can help you transfer your property back to the lender, potentially avoiding a lengthy foreclosure process. Follow the steps below to complete the form accurately.

After submitting the form, the lender will review it. They may reach out for additional information or clarification. Once everything is approved, the transfer of property will be processed, and you will receive confirmation from the lender.

Filling out and using the New York Deed in Lieu of Foreclosure form can be a significant step for homeowners facing foreclosure. Here are some key takeaways to keep in mind:

Being informed and prepared can make a significant difference in how you approach this challenging situation.

Deed in Lieu of Foreclosure Pa - The documentation must be completed accurately to ensure a valid transfer of ownership.

Deed in Lieu of Foreclosure Vs Foreclosure - Borrowers can often stay in their home until the lender finalizes the property transfer.

For those seeking to obtain a death certificate in New York City, the NYC Health VR 66 form is essential. Applicants must ensure they provide accurate details about both the deceased and themselves while adhering to the guidelines for identification and documentation. To facilitate the application process, resources are available, including NY PDF Forms, which offer a structured format to streamline this important request.

What Does an Arizona Homeowner Lose When Choosing to Use Deed in Lieu of Foreclosure? - The process is typically confidential, allowing for a smoother transition without public foreclosure proceedings.

A Deed in Lieu of Foreclosure is a legal document that allows a borrower to transfer ownership of their property to the lender to avoid foreclosure. This process often involves several other forms and documents that help facilitate the transaction and protect the interests of both parties. Below is a list of commonly used documents associated with this process.

Understanding these documents can help ensure a smoother process when navigating a deed in lieu of foreclosure. Each document plays a crucial role in protecting the rights and responsibilities of both the borrower and the lender.

A Deed in Lieu of Foreclosure is a legal agreement where a homeowner voluntarily transfers the ownership of their property to the lender to avoid the lengthy and costly process of foreclosure. This option can be beneficial for both parties, as it allows the homeowner to walk away from the mortgage obligation and the lender to take possession of the property without going through court proceedings.

Eligibility for a Deed in Lieu of Foreclosure typically depends on several factors:

Each lender may have specific criteria, so it’s essential to check with them directly.

Opting for a Deed in Lieu of Foreclosure can offer several advantages:

Completing a Deed in Lieu of Foreclosure involves several key steps:

Once the Deed in Lieu of Foreclosure has been signed and recorded, it is generally considered a final agreement. This means that the homeowner cannot simply change their mind and retain ownership of the property. However, it’s crucial to fully understand the implications and explore all options before proceeding. Consulting with a legal or financial advisor can help clarify any uncertainties and ensure that this is the right choice for your situation.