Printable Loan Agreement Template for New York

Printable Loan Agreement Template for New York

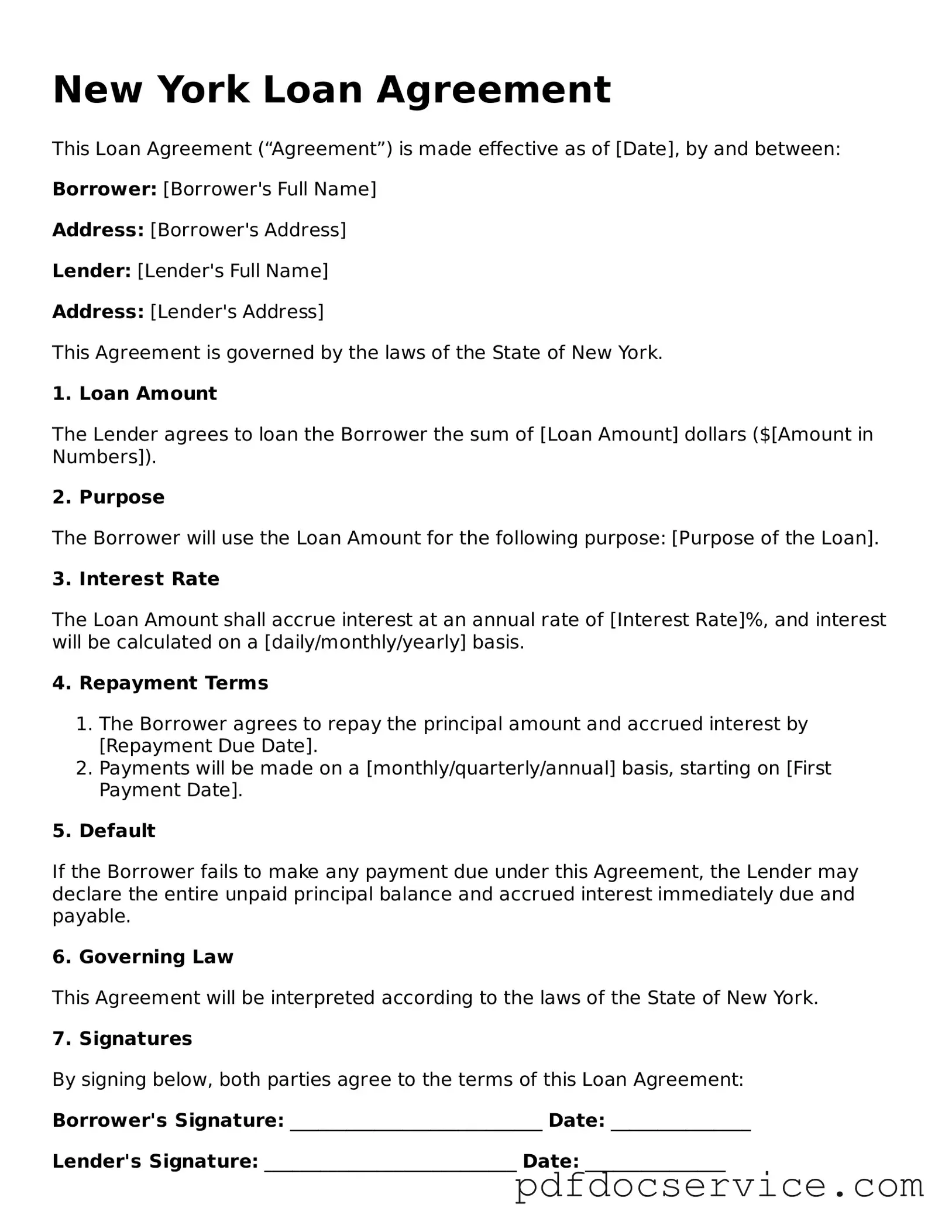

The New York Loan Agreement form is a crucial document for anyone looking to formalize a loan arrangement in the state. It serves as a clear outline of the terms and conditions agreed upon by the lender and the borrower. Key aspects of the form include the loan amount, interest rate, repayment schedule, and any collateral involved. Additionally, it specifies the rights and responsibilities of both parties, ensuring that expectations are set from the outset. This form also addresses potential default scenarios, detailing what happens if the borrower fails to meet their obligations. By clearly laying out these elements, the New York Loan Agreement helps to protect both the lender’s and borrower’s interests, fostering a transparent and trustworthy lending environment.

Promissory Note: A promissory note is a written promise to pay a specific amount of money at a defined time. Like a loan agreement, it outlines the terms of repayment, including interest rates and due dates. Both documents serve as evidence of a debt.

Mortgage Agreement: A mortgage agreement secures a loan with real property. Similar to a loan agreement, it details the obligations of the borrower, including payment schedules and consequences of default. Both documents establish the lender's rights in case of non-payment.

Lease Agreement: A lease agreement outlines the terms under which one party rents property from another. Both lease and loan agreements specify payment amounts, duration, and conditions for termination. They create a legal obligation between the parties involved.

Credit Agreement: A credit agreement governs the terms of borrowing under a credit facility. It is similar to a loan agreement in that it defines the amount borrowed, interest rates, and repayment terms. Both documents aim to protect the lender's interests while providing clarity to the borrower.

Personal Guarantee: A personal guarantee is a promise made by an individual to repay a loan if the primary borrower defaults. Like a loan agreement, it outlines the obligations of the guarantor and provides security for the lender, ensuring that there is recourse if the borrower fails to meet their obligations.

Security Agreement: A security agreement creates a security interest in personal property to secure a loan. Similar to a loan agreement, it details the terms of the loan and the collateral involved. Both documents are crucial in establishing the lender's rights over the collateral in case of default.

Debt Settlement Agreement: A debt settlement agreement is a contract between a debtor and creditor to settle a debt for less than the full amount owed. Like a loan agreement, it outlines terms and conditions, including payment schedules and amounts. Both agreements aim to resolve financial obligations amicably.

| Fact Name | Description |

|---|---|

| Purpose | The New York Loan Agreement form outlines the terms and conditions of a loan between a lender and a borrower. |

| Governing Law | This agreement is governed by the laws of the State of New York. |

| Loan Amount | The form specifies the exact amount of money being borrowed, which is crucial for both parties. |

| Interest Rate | The interest rate applicable to the loan is clearly stated, ensuring transparency in repayment obligations. |

| Repayment Terms | It details the repayment schedule, including the frequency and amount of payments due. |

| Default Clauses | The agreement includes provisions that outline the consequences if the borrower defaults on the loan. |

| Signatures | Both parties must sign the agreement to validate it, indicating their acceptance of the terms. |

Filling out the New York Loan Agreement form is a straightforward process. By following the steps below, you can ensure that all necessary information is accurately provided. This will help facilitate a smooth transaction between the lender and borrower.

When filling out and using the New York Loan Agreement form, consider the following key takeaways:

Sample Promissory Note California - It facilitates record-keeping of financial transactions.

For those looking to navigate the requirements of plumbing work in the city, the NYC Buildings OP128 form serves as an essential tool. This form enables licensed master plumbers to report ordinary plumbing tasks without the need for a permit. For additional resources, you can refer to NY PDF Forms which can provide further guidance on the documentation process, ensuring compliance with regulations outlined in the Administrative Code 28-105.4.4.

Maryland Promissory Note - Outlines conditions under which the loan may be modified or terminated.

When entering into a loan agreement in New York, several other documents may be necessary to ensure clarity and compliance. These documents can help outline terms, provide security, and protect the interests of both parties involved in the transaction.

These documents work together with the Loan Agreement to create a comprehensive framework for the loan transaction. Each serves a specific purpose, contributing to a clear understanding of the obligations and rights of both parties.

A New York Loan Agreement is a legal document that outlines the terms and conditions under which a borrower receives funds from a lender. This agreement specifies the amount borrowed, interest rates, repayment schedule, and any collateral involved. It serves to protect both parties by clearly defining their rights and obligations.

Anyone who is borrowing or lending money in New York should consider using a Loan Agreement. This includes individuals, businesses, and organizations. Having a formal agreement helps prevent misunderstandings and provides a clear record of the transaction.

A comprehensive Loan Agreement typically includes the following components:

While verbal agreements can be legally binding, having a written Loan Agreement is highly recommended. A written document provides clear evidence of the terms agreed upon and can be crucial in case of disputes. It also helps both parties understand their responsibilities.

Yes, a Loan Agreement can be modified if both parties agree to the changes. It is advisable to document any modifications in writing and have both parties sign the updated agreement to ensure clarity and enforceability.

If the borrower fails to meet the repayment terms, the lender has several options. These may include:

It is important to refer to the default terms specified in the Loan Agreement for guidance.

In New York, a Loan Agreement does not need to be notarized to be valid. However, certain types of loans, such as those involving real estate, may have additional requirements. It is wise to ensure compliance with all applicable laws and regulations.

Yes, a properly executed Loan Agreement can be enforced in court. If a dispute arises, either party can bring the matter before a judge. The agreement will serve as evidence of the terms agreed upon, making it easier to resolve the issue.

If you have questions or concerns regarding your Loan Agreement, consider consulting a legal professional. They can provide guidance tailored to your specific situation and help ensure that your rights are protected.