Printable Promissory Note Template for New York

Printable Promissory Note Template for New York

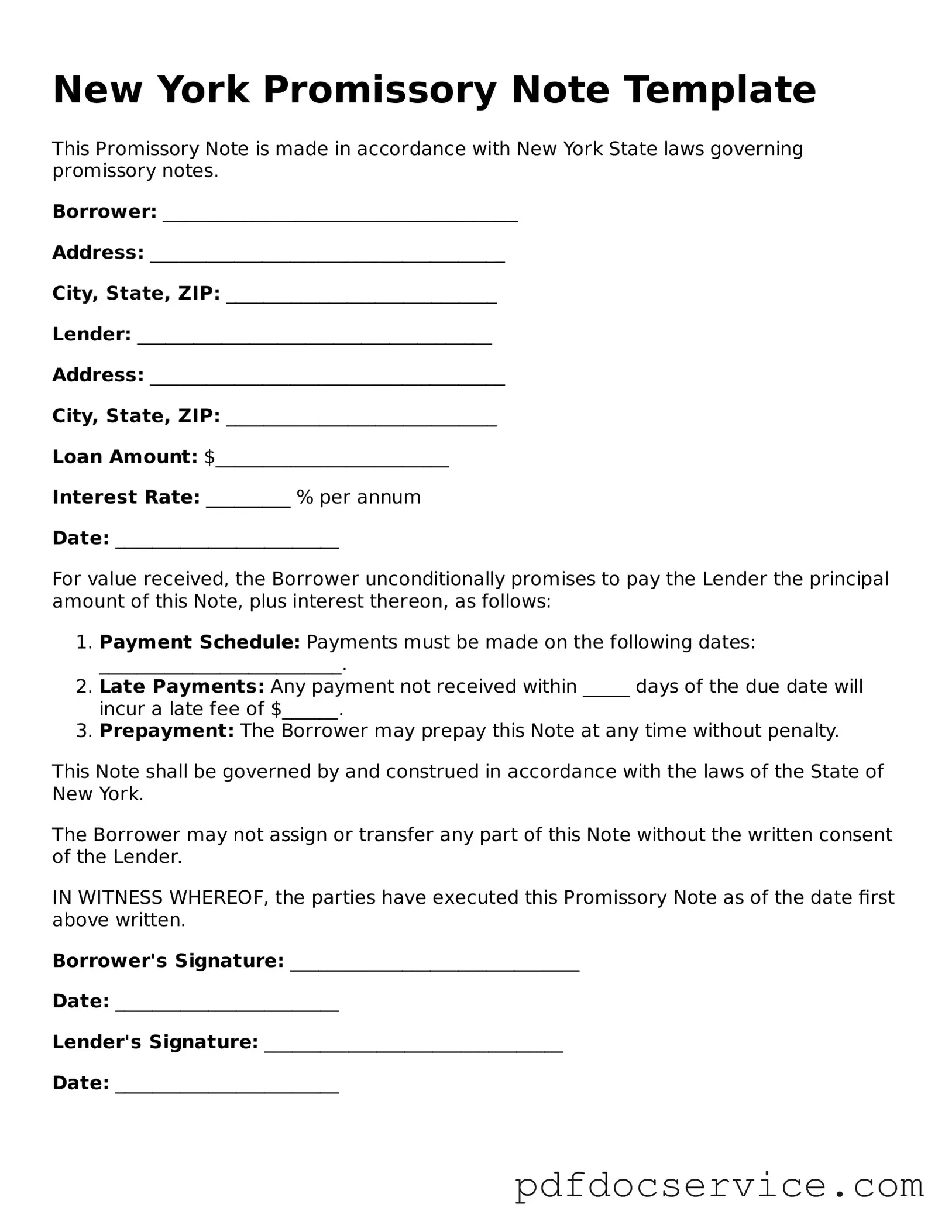

In the realm of financial transactions, the New York Promissory Note serves as a crucial instrument for establishing a clear agreement between a borrower and a lender. This legally binding document outlines the terms under which a borrower agrees to repay a specific sum of money to the lender, including the interest rate, repayment schedule, and any applicable fees. It is essential for both parties to understand the implications of this note, as it not only provides a framework for repayment but also protects the rights of the lender while ensuring the borrower is fully aware of their obligations. The Promissory Note form typically includes vital details such as the names and addresses of both parties, the principal amount borrowed, and the due date for repayment. Additionally, it may specify the consequences of default, offering clarity on what actions can be taken should the borrower fail to meet their obligations. By comprehensively addressing these aspects, the New York Promissory Note fosters transparency and trust, making it an indispensable tool in personal and business financing.

Promissory Note Form: For those entering loan agreements in Arizona, the comprehensive Promissory Note form guidelines provide essential information for creating clear and binding contracts.

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money at a designated time or on demand. |

| Governing Law | In New York, promissory notes are governed by the Uniform Commercial Code (UCC) Article 3. |

| Parties Involved | The note typically involves two parties: the maker (who promises to pay) and the payee (who receives the payment). |

| Requirements | A valid promissory note must include the amount to be paid, the interest rate (if any), and the payment schedule. |

| Signature | The maker must sign the note for it to be legally binding. An electronic signature is also acceptable under New York law. |

| Enforceability | Promissory notes are legally enforceable documents, meaning the payee can take legal action if the maker fails to pay. |

| Transferability | Promissory notes can often be transferred to another party, allowing the new holder to collect payment. |

Once you have the New York Promissory Note form in front of you, it's time to provide the necessary information to make it complete. This document will outline the terms of the loan and the obligations of both the borrower and the lender. Follow these steps carefully to ensure that all required information is accurately filled out.

After completing the form, review it carefully to ensure all information is correct. Once everything is in order, both parties should keep a copy for their records. This will help in maintaining clarity and accountability throughout the duration of the loan.

The New York Promissory Note is a legal document that outlines a borrower's promise to repay a loan under specified terms.

It is essential to include the principal amount, interest rate, and repayment schedule to ensure clarity for both parties.

Both the lender and borrower must sign the document to make it legally binding.

In New York, a Promissory Note can be secured or unsecured, depending on whether collateral is involved.

It is advisable to keep a copy of the signed Promissory Note for personal records and future reference.

If disputes arise, the Promissory Note can serve as evidence in court to enforce repayment terms.

Simple Promissory Note - It's beneficial to involve a witness when signing the Promissory Note.

A Power of Attorney form is a legal document that allows one person to act on behalf of another in legal or financial matters. This form grants the appointed individual the authority to make decisions for the person who created it, often called the principal. For more information on creating this important document, you can visit mypdfform.com/blank-power-of-attorney/. Understanding the Power of Attorney is essential for making informed choices about personal and financial affairs.

Tennessee Promissory Note - Each promissory note should address what will happen in the case of unforeseen hardships.

Texas Promissory Note Form - The note can be used for personal loans, business funding, or real estate transactions.

When dealing with a New York Promissory Note, several other documents may be necessary to ensure a smooth transaction. Each document serves a specific purpose and helps clarify the terms of the agreement between the parties involved. Here’s a list of forms you might encounter alongside a Promissory Note.

Understanding these documents can help you navigate the lending process more effectively. Each form plays a crucial role in protecting the interests of both the borrower and the lender, ensuring clarity and compliance throughout the transaction.

A New York Promissory Note is a legal document that outlines a borrower's promise to repay a loan to a lender. It specifies the amount borrowed, the interest rate, repayment schedule, and any consequences for defaulting on the loan. This document serves as a formal agreement between the parties involved.

Any individual or business can use a Promissory Note in New York. This includes personal loans between friends or family members, as well as formal agreements between businesses. It is important that both parties understand the terms and conditions laid out in the note.

A typical Promissory Note will include:

Yes, a properly executed Promissory Note is legally binding. Both parties must agree to the terms and sign the document for it to be enforceable in a court of law. It is advisable to have witnesses or notarization to strengthen the validity of the note.

Yes, a Promissory Note can be modified if both the borrower and lender agree to the changes. It is essential to document any modifications in writing and have both parties sign the updated agreement. This helps prevent misunderstandings in the future.

If the borrower defaults, the lender may take several actions. These can include:

Defaulting can also lead to damage to the borrower’s credit score and may result in the loss of collateral if one was specified in the note.

While it is not legally required to have a lawyer draft a Promissory Note, consulting with one can provide valuable guidance. A legal professional can ensure that the document meets all necessary requirements and protects your interests. For straightforward loans, many templates are available online.

The duration of a Promissory Note depends on the repayment terms agreed upon by both parties. Some notes may be due in a few months, while others may extend over several years. It is crucial to clearly state the maturity date in the document.

Yes, a Promissory Note can be transferred or assigned to another party, unless the note specifically states otherwise. This process typically requires the original lender to notify the borrower of the transfer. The new holder then assumes the rights to collect the debt under the same terms.

A Promissory Note is a simpler document that primarily focuses on the borrower's promise to repay the loan. In contrast, a loan agreement is more comprehensive and includes detailed terms regarding the loan, such as covenants, representations, and warranties. While both documents serve to formalize a loan, the loan agreement provides a broader framework for the relationship between the parties.