Fill Your Profit And Loss Form

Fill Your Profit And Loss Form

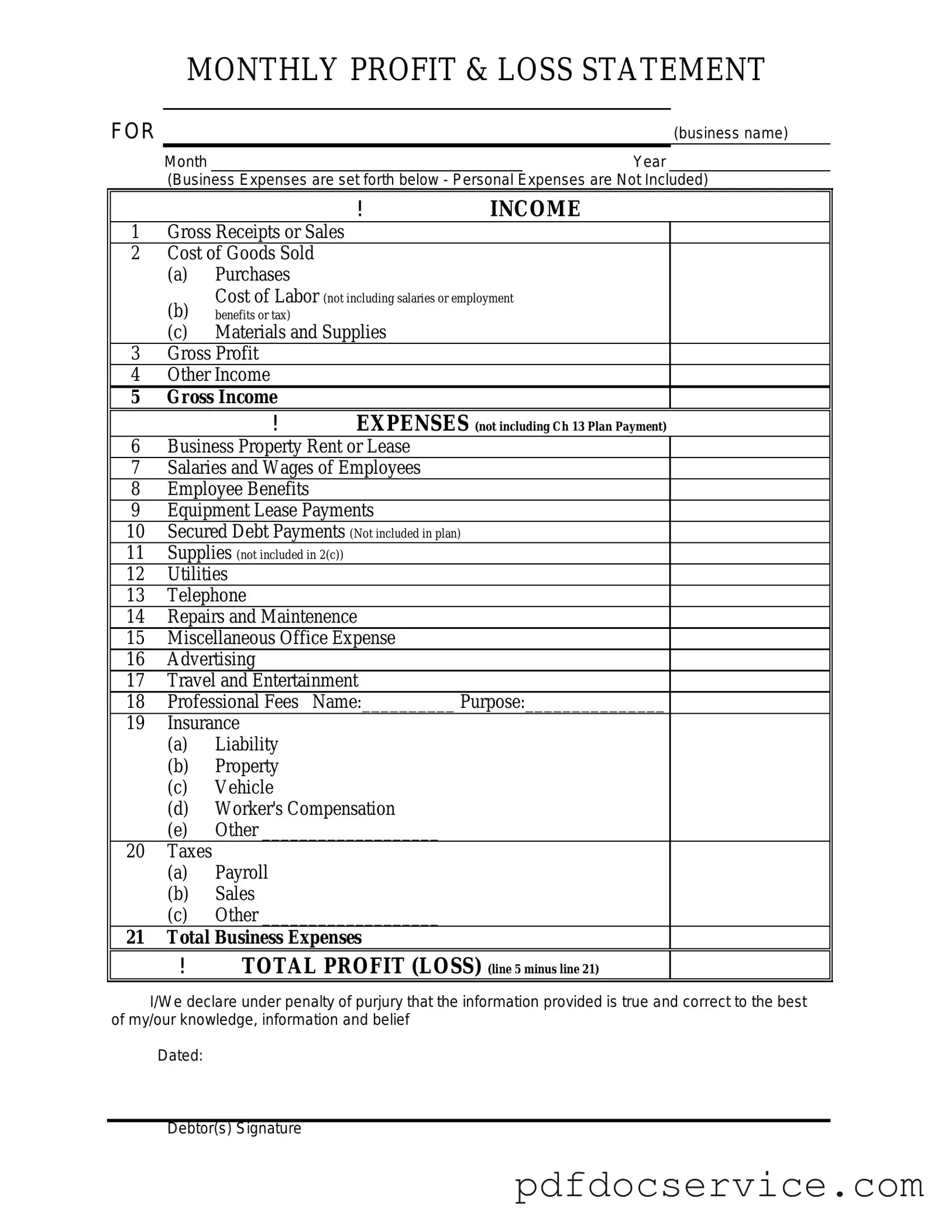

The Profit and Loss form, often referred to as the P&L statement, plays a critical role in understanding a business's financial performance over a specific period. This document summarizes revenues, costs, and expenses, providing a clear picture of whether the business is operating at a profit or a loss. Key components of the form include total revenue, which reflects all income generated from sales, and cost of goods sold, which indicates the direct costs associated with producing those goods. Operating expenses, such as rent, utilities, and salaries, are also detailed, showcasing the ongoing costs of running the business. Additionally, the form may include non-operating income and expenses, allowing for a comprehensive view of all financial activities. Ultimately, the Profit and Loss form serves as an essential tool for business owners, investors, and stakeholders to assess profitability and make informed decisions regarding future operations and investments.

| Fact Name | Description |

|---|---|

| Purpose | The Profit and Loss form is used to summarize a company's revenues, costs, and expenses during a specific period, providing insight into its financial performance. |

| Components | This form typically includes sections for total revenue, cost of goods sold, gross profit, operating expenses, and net profit or loss. |

| State-Specific Forms | Some states may have specific requirements for Profit and Loss forms, governed by state tax laws or regulations. |

| Filing Requirements | Businesses may be required to submit Profit and Loss forms annually or quarterly, depending on their structure and state laws. |

Completing the Profit and Loss form requires careful attention to detail. This process helps you track your financial performance over a specific period. Follow these steps to ensure you fill out the form correctly.

Once you have filled out the Profit and Loss form, you can use the information to analyze your business's financial health. This data will assist in making informed decisions moving forward.

Filling out and using a Profit and Loss (P&L) form is essential for understanding a business's financial performance. Here are some key takeaways to consider:

1099 Nec Forms - All relevant instructions can be found on the IRS website.

State Disability Insurance - Accurate information on the DE 2501 directly impacts the success of your claim.

The Profit and Loss form is a vital document for assessing a business's financial performance over a specific period. To get a comprehensive view of a company's financial health, several other forms and documents are commonly used alongside it. Below is a list of these essential documents, each serving a unique purpose.

By utilizing these documents in conjunction with the Profit and Loss form, businesses can gain a clearer understanding of their financial position, enabling better decision-making and strategic planning.

The Profit and Loss form is a financial document that summarizes the revenues, costs, and expenses incurred during a specific period. It provides a clear overview of a business's financial performance, allowing stakeholders to assess profitability and operational efficiency. This form is crucial for tracking income and expenditures, making it easier to identify trends over time.

The Profit and Loss form is important for several reasons:

The frequency of completing a Profit and Loss form can vary based on the needs of the business. Common practices include:

Ultimately, businesses should choose a frequency that aligns with their operational needs and reporting requirements.

A Profit and Loss form generally includes the following sections:

Using the Profit and Loss form can help improve a business in various ways:

Regularly reviewing this form can lead to better financial management and strategic planning.