Blank Promissory Note Form

Blank Promissory Note Form

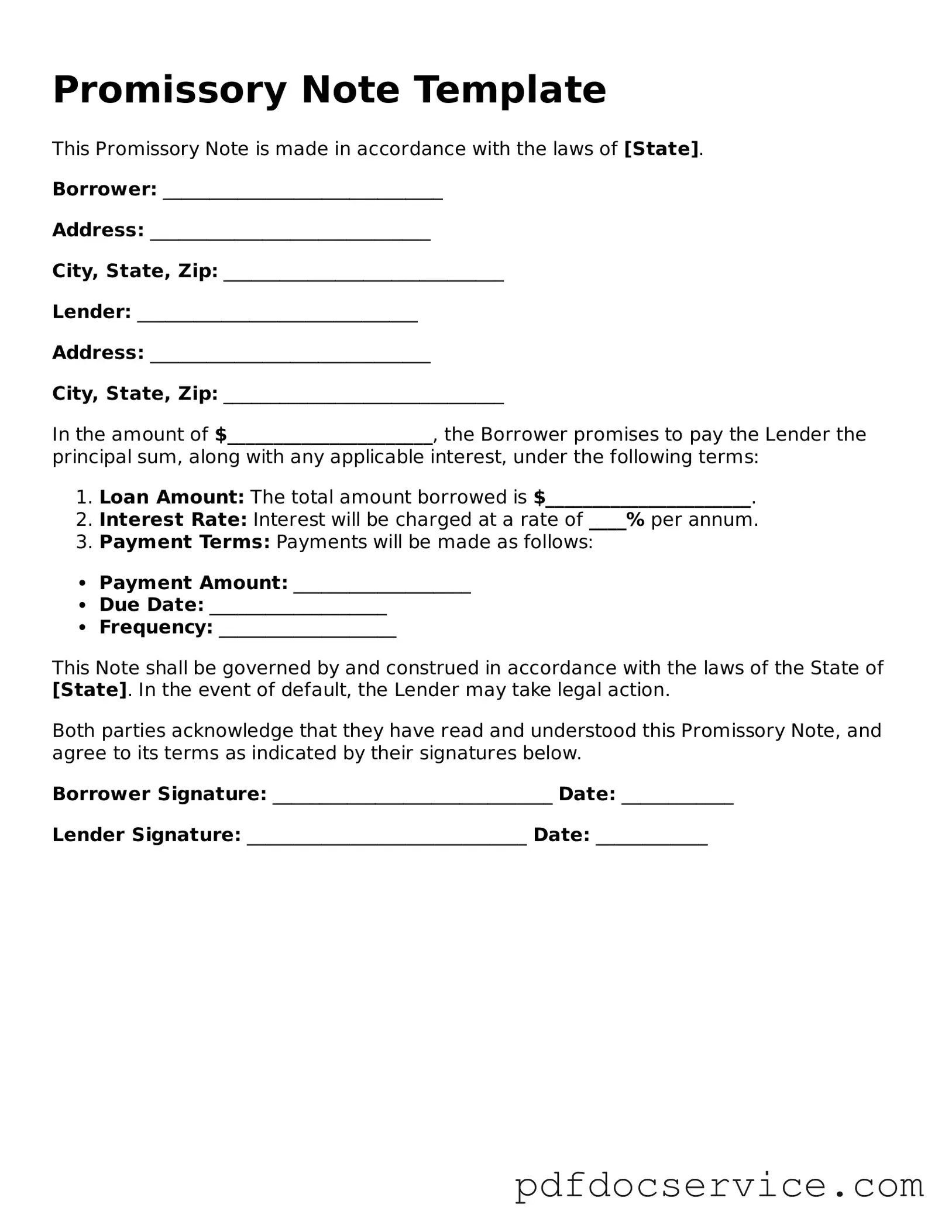

When entering into a financial agreement, clarity and security are paramount. A Promissory Note serves as a vital document in such transactions, outlining the terms under which one party agrees to pay a specified sum of money to another. This form typically includes essential details such as the principal amount, interest rate, payment schedule, and the maturity date. It also specifies the rights and obligations of both the lender and the borrower, ensuring that each party understands their commitments. In addition to these fundamental elements, the Promissory Note may include provisions for late fees, prepayment options, and what happens in the event of default. By clearly delineating these aspects, the form not only protects the interests of the lender but also provides the borrower with a transparent understanding of their financial responsibilities. Understanding the intricacies of this document is crucial for anyone involved in lending or borrowing money, as it lays the groundwork for a legally binding agreement that can help prevent disputes and misunderstandings down the line.

A Promissory Note is a crucial financial document that outlines a promise to pay a specific amount of money at a designated time. However, it shares similarities with several other documents. Here are six documents that are akin to a Promissory Note:

Understanding these documents can help individuals navigate financial agreements more effectively. Each serves a unique purpose, yet they all share the common thread of establishing financial obligations and commitments.

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person at a specified time. |

| Key Elements | It must include the principal amount, interest rate, maturity date, and the signatures of the borrower and lender. |

| Governing Law | In the United States, promissory notes are primarily governed by the Uniform Commercial Code (UCC) and state-specific laws. |

| Enforceability | A promissory note is enforceable in court, provided it meets all legal requirements and is properly executed. |

After obtaining the Promissory Note form, you will need to complete it carefully to ensure all necessary information is provided. This document will require specific details about the loan agreement, including the parties involved, the amount borrowed, and the repayment terms.

When filling out and using a Promissory Note form, consider these key takeaways:

How to Get Acord Insurance Certificate - The Acord 50 WM is integral in managing a business’s insurance liabilities.

Better Business Reviews - Account information was mishandled or exposed.

In situations where you need to formally address unwarranted actions, utilizing a legal document such as a cease and desist letter is essential. The Texas Cease and Desist Letter form plays a crucial role in ensuring that your rights are protected under Texas law. This particular template can be customized to your specific needs, making it easier to communicate your demands clearly. For those looking to obtain this document, you can find the necessary resources online, including the option to access Texas PDF Forms for a streamlined experience.

Aia Document A305 - Used by architects and owners to evaluate contractor qualifications.

A Promissory Note is a crucial document in financial transactions, serving as a written promise to repay a loan under specified terms. However, it often accompanies other forms and documents that help clarify the agreement and protect the interests of both parties. Here are four common documents that are frequently used alongside a Promissory Note:

Understanding these documents is essential for anyone entering into a loan agreement. They provide clarity and protection, ensuring that all parties are aware of their rights and responsibilities. By using these forms in conjunction with a Promissory Note, borrowers and lenders can create a solid foundation for their financial relationship.

A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a particular time or on demand. It serves as a legal document that outlines the terms of the loan, including the principal amount, interest rate, payment schedule, and any penalties for late payments. This document can be used in various financial transactions, including personal loans, business loans, and real estate transactions.

Several essential elements must be included in a promissory note to ensure its validity:

A promissory note is a legally binding contract. If the borrower fails to make the required payments, the lender has the right to take legal action to enforce the terms of the note. This may involve filing a lawsuit to recover the owed amount. Courts generally uphold the terms of a promissory note as long as it meets the necessary legal requirements, such as being signed by both parties and containing clear terms.

Yes, a promissory note can be transferred or sold to another party. This process is known as "negotiation." When a promissory note is transferred, the new holder assumes the rights to receive payments under the terms of the note. However, it is important to note that the borrower must be informed of the transfer, and the terms of the note should allow for such a transfer. Additionally, the transfer should be documented properly to avoid disputes in the future.